Get Quotes

5MinuteInsure.com is not yet available in your area. Check back

soon!

This article has been reviewed by licensed insurance industry expert Moshe Fishman on July 28, 2023

Does getting older mean higher car insurance rates? A driver’s age does matter when it comes to buying auto insurance and seniors are no exception. They will likely see their insurance premiums slowly increase as they age, particularly after 65 years old. So, although a 60-year old driver may be happy to experience slightly lower premiums, by the age of 70 senior citizens will notice higher rates.

In fact, age is high on the list of factors that determine what you’ll pay for car insurance. Even though safe driving seniors may drive less, they will still need to buy minimum liability coverage effective in their state of residence.

According to the Insurance Information Institute, this minimum coverage will provide some protection to cover another’s vehicle or injuries if you cause an accident. But it’s not sufficient coverage and can leave you vulnerable to financial hardship. Remember, the cheapest car insurance for seniors is not necessarily the best car insurance for seniors.

Unfortunately, premiums do slowly rise once you hit age 65, and looking at better coverages can be costly. As a senior, however, you can shop and compare available policies to be sure you are getting the best rates for your car insurance.

What this article covers:

What you should know:

Using a reliable online website to make comparisons of rates is a good place to start. They can do the legwork for you and give you the best possible options. Their relationship with insurers is based on a mutual goal to provide customers with fair pricing that reflects each driver’s situation.

Insurance carriers have varying rates so getting quotes from different companies is a logical step in buying your car insurance. But it’s important to remember that it’s not always just about the price, it’s also about customer satisfaction. That becomes especially important if you or someone driving your car has an accident while on the road and you need to make a claim. After all, that’s why you purchase insurance in the first place—to be financially protected if an incident occurs.

For example, J.D. Power’s 2021 U.S. Auto Claims Satisfaction Study ranks insurers like Nationwide, Safeco, Travelers, Allstate, and Progressive among those receiving high scores in overall customer satisfaction. The study was based on 7,345 car insurance customers who settled their claim within the prior six months before the survey.

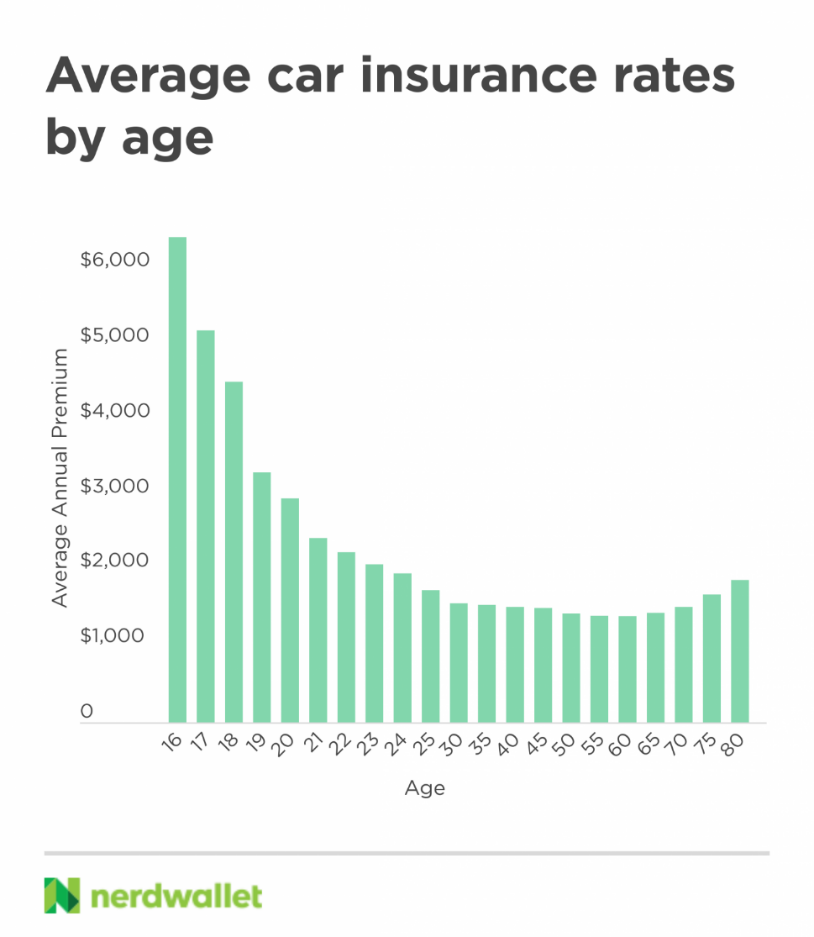

As we age, what we can expect to pay for car insurance resembles a roller coaster. As a teen, you start out with huge premiums largely due to a lack of experience behind the wheel. Teens are also a high risk for accidents. According to NerdWallet’s Average Annual Premium estimates, these rates can hover in the thousands when you’re 16 years old, drop slowly, and eventually crawl back up when you are a senior.

But it’s not just about your age. There are considerations like driving record, location, annual mileage, vehicle type, and other factors that will dictate what your coverages will cost.

In addition, the more coverages you choose, the higher the limits, and your deductibles will all contribute to what you can expect to pay. The more coverage you buy, the greater the protection for you, your passengers, other drivers, your car, and other vehicles and property.

Here are the annual average premiums for full and minimum coverages for 60+ year-old drivers based on gender:

| Full Coverage | Male | Female |

| 60 years old | $1,420 | $1,419 |

| 65 years old | $1,468 | $1,457 |

| 70 years old | $1,551 | $1,532 |

| 75 years old | $1,741 | $1,671 |

| 80 years old | $1,962 | $1,836 |

| Minimum Coverage | Male | Female |

| 60 years old | $529 | $534 |

| 65 years old | $554 | $556 |

| 70 years old | $595 | $592 |

| 75 years old | $676 | $656 |

| 80 years old | $775 | $731 |

Another key factor that affects what seniors will pay for auto coverage depends on the state in which they live. This is true of minimum state requirements as well as full coverage costs.

State rates can vary widely due to their approach to insurance laws. These differences in laws are what decide the costs. Michigan, Nevada, and Rhode Island are among those states with the priciest rates.

Here are the average annual rates for seniors by state that include comp and collision, 100/300/100 liability:

| State | Age 60 | Age 65 | Age 70 | Age 75 |

| Alaska | $1,280 | $1,383 | $1,471 | $1,630 |

| Alabama | $1,444 | $1,473 | $1,548 | $1,739 |

| Arkansas | $1,521 | $1,585 | $1,679 | $1,920 |

| Arizona | $1,582 | $1,657 | $1,730 | $1,956 |

| California | $1,660 | $1,645 | $1,786 | $1,930 |

| Colorado | $1,742 | $1,769 | $1,821 | $1,965 |

| Connecticut | $1,703 | $1,751 | $1,866 | $2,163 |

| District of Columbia | $1,928 | $1,991 | $2,087 | $2,342 |

| Delaware | $1,741 | $1,803 | $1,893 | $2,150 |

| Florida | $1,873 | $1,922 | $1,996 | $2,248 |

| Georgia | $1,611 | $1,667 | $1,765 | $2,019 |

| Hawaii | $1,594 | $1,594 | $1,594 | $1,594 |

| Iowa | $1,119 | $1,138 | $1,192 | $1,313 |

| Idaho | $1,062 | $1,127 | $1,176 | $1,391 |

| Illinois | $1,274 | $1,308 | $1,365 | $1,526 |

| Indiana | $1,072 | $1,079 | $1,147 | $1,286 |

| Kansas | $1,405 | $1,443 | $1,471 | $1,676 |

| Kentucky | $2,070 | $2,146 | $2,256 | $2,560 |

| Louisiana | $2,322 | $2,435 | $2,417 | $2,407 |

| Massachusetts | $1,369 | $1,050 | $1,109 | $1,168 |

| Maryland | $1,708 | $1,861 | $1,954 | $1,954 |

| Maine | $947 | $941 | $945 | $938 |

| Michigan | $3,084 | $3,171 | $3,473 | $3,915 |

| Minnesota | $1,337 | $1,407 | $1,453 | $1,642 |

| Missouri | $1,493 | $1,518 | $1,573 | $1,731 |

| Mississippi | $1,380 | $1,416 | $1,479 | $1,731 |

| Montana | $1,741 | $1,830 | $1,898 | $2,255 |

| North Carolina | $1,293 | $1,324 | $1,392 | $1,443 |

| North Dakota | $1,236 | $1,258 | $1,299 | $1,426 |

| Nebraska | $1,265 | $1,285 | $1,404 | $1,557 |

| New Hampshire | $950 | $992 | $1,049 | $1,166 |

| New Jersey | $1,729 | $1,756 | $1,761 | $1,934 |

| New Mexico | $1,387 | $1,441 | $1,521 | $1,747 |

| Nevada | $2,149 | $2,185 | $2,313 | $2,645 |

| New York | $1,876 | $1,935 | $2,028 | $2,266 |

| Ohio | $1,017 | $1,049 | $1,100 | $1,233 |

| Oklahoma | $1,591 | $1,596 | $1,633 | $1,766 |

| Oregon | $1,350 | $1,361 | $1,420 | $1,594 |

| Pennsylvania | $1,448 | $1,476 | $1,574 | $1,768 |

| Rhode Island | $1,992 | $2,401 | $2,428 | $2,472 |

| South Carolina | $1,363 | $1,432 | $1,500 | $1,727 |

| South Dakota | $1,298 | $1,339 | $1,365 | $1,522 |

| Tennessee | $1,227 | $1,323 | $1,467 | $1,767 |

| Texas | $1,586 | $1,674 | $1,750 | $1,920 |

| Utah | $1,311 | $1,343 | $1,400 | $1,596 |

| Virginia | $996 | $1,063 | $1,132 | $1,275 |

| Vermont | $1,183 | $1,242 | $1,307 | $1,493 |

| Washington | $1,395 | $1,446 | $1,520 | $1,666 |

| Wisconsin | $1,124 | $1,145 | $1,193 | $1,330 |

| West Virginia | $1,415 | $1,467 | $1,530 | $1,752 |

| Wyoming | $1,445 | $1,494 | $1,572 | $1,785 |

Let your insurer know if you have a senior in your household who drives, particularly if they will be driving your car. If they have their own vehicle and policy, you may not have to add them to your policy, but your insurance company may request proof of their insurance.

But if there is a senior (aging parent or other) who lives with you and they do not have their own vehicle or car insurance, you will need to add them to your policy. This is especially true if they plan to drive your car. The worst-case scenario would be if they are involved in an accident driving your vehicle and not covered in your policy. Results could be disastrous and include having a claim be denied, losing your coverage, and paying huge expenses out of your own pocket.

If you do add a senior to your policy, be aware of warning signs that indicate it may be time to stop driving altogether. AARP provides a list of things to watch out for and how to discuss the signs of unsafe driving.

Aside from age, seniors should be aware that there are other factors that insurance companies consider when determining rates. And although age is at the top of the list, other circumstances also make a difference.

Where you live, particularly in what state, dictates what your minimum required coverages will be and vary from one state to the next. Your location and other rating factors that affect insurance rates are usually broken out into two main categories that include Non-Driving Factors and Driving/Car-Related Factors.

State and Zip Code: The state in which you live, as well as your vehicle, is a key factor in determining coverage costs. Extreme weather (tornadoes, hail, hurricanes) and whether you live in a rural or urban area can have an influence on your rates. In addition, states have different laws and minimum insurance requirements that dictate what you can expect to pay.

Age: Most states allow insurers to use age as a rating factor. In doing so, both teenage and senior drivers are within the highest risk categories. According to WalletHub auto coverage rates can vary greatly based on age, up to 367%.

Age can have the biggest impact on costs depending on how old you are. For example, teenagers are considered a higher risk due to their inexperience as they lack driving time on the road and in different situations. They are also more likely to be involved in a crash, as much as three times more likely to get into an accident than 20+ year-olds according to the Insurance Institute for Highway Safety.

Seniors are also considered higher risk even though they have plenty of experience behind the wheel. Depending on age, the National Institute of Aging reports that seniors may experience slower reaction times and reflexes, poorer vision, decreased hearing, cognitive decline, and decreased motor skills. Medications can also play a role, although this can be a negative influence at any age.

It’s worth noting that there are very few states where your age will not directly affect what you will pay including California, Hawaii, and Massachusetts. These states do not permit insurance companies to factor in a driver’s age in their rates.

| Average Annual Miles per Driver by Age | ||

| Age | Female | Male |

| 16-19 | 6,873 | 8,206 |

| 20-34 | 12,004 | 17,976 |

| 35-54 | 11,464 | 18,858 |

| 55-64 | 7,780 | 15,859 |

| 65+ | 4,785 | 10,304 |

| Average | 10,142 | 16,550 |

Source: Federal Highway Administration

Gender: Not all states allow gender to be used in calculating insurance costs. California, Hawaii, Massachusetts, Michigan, Montana, North Carolina, and Pennsylvania ban the use of gender to determine coverage rates in their states. But in other states, teenage males may find themselves paying the highest rates but eventually pay less than women drivers at around age 45.

Looking at the overall picture, The National Highway Traffic Safety Administration has shown that men are responsible for 6.1 million crashes annually versus women at 4.4 million per year. Their study shows, “The fatality rate per 100,000 population was lower for females than for males in 2019…”

To help explain some of the differences, Insurance Institute for Highway’s article, Fatality Facts Males and Females 2019 states that males have been shown to drive more miles and are more likely to participate in riskier behavior (drinking while driving, speeding, etc.).

Credit History: Bottom line, according to insurers, is that a driver with a low credit score is more likely to make a claim. As a result, this makes them a higher risk and can increase costs. This is true in most states, but not all. California, Hawaii, and Massachusetts do not allow insurers to use credit ratings to determine premiums.

Marital Status: Being married typically means reduced auto insurance rates. According to DMV.org, a married person is less likely to be in an accident than a single person. When determining rates, however, the driving records of both partners will be considered and reflected in your premium.

Some states do not allow insurers to factor in marital status including Hawaii, Massachusetts, and Michigan. Once you become single (lose your spouse or get divorced), you will move into the single status category and your rates may then increase.

Driving Record: If you have a clean driving record, you will pay less in premiums than a driver with a poor driving history. In addition, the number of years you’ve been driving also helps reduce rates. But eventually, the rates can creep back up for seniors as they get older.

High-Risk Violations: Car crashes and ticket violations can increase your insurance rates. The more severe the violation the more your cost for coverage will likely increase. Being a repeat offender and getting multiple violations can also peg you as a high-risk driver. Some insurance carriers consider these violations in determining your insurance costs for three years or more.

Annual Mileage: The more miles you drive the greater the risk you pose, which then equates to higher premiums. So, if you are still commuting daily to work, you could pay more. The opposite also holds true. If you are retired, for example, and you find yourself driving less, it’s a good idea to let your insurer know as you may benefit from reduced premiums.

Vehicle Make/Model: Insurers will also look at your vehicle’s value, type (truck, car, SUV, etc.), and popularity with thieves as a factor in figuring your insurance costs. Full-size Ford trucks and Honda Accords, for example, are a favorite target for theft. Safety features are also considered, so hanging on to that older car lacking these features could possibly cost you more in insurance. The amount your vehicle will cost to repair if involved in an accident is yet another consideration.

Insurance and Claims History: Maintaining insurance on your vehicle and not having a lapse of coverage can help keep your premiums in check. If you have not made any claims in the last few years, you could benefit from a discount. If, on the other hand, you’ve been involved in accidents over the past several years, higher premiums may be the result. The higher rates reflect that insurance companies see you as a bigger risk when driving.

Nobody wants to pay more in auto insurance if they don’t have to and seniors are no exception. Just because you age doesn’t mean you can’t find ways to save on your premiums. Here are some things seniors and others can do to grab discounts.

For other answers to your important insurance questions, check our FAQs page.