Get Quotes

5MinuteInsure.com is not yet available in your area. Check back

soon!

This article has been reviewed by licensed insurance industry expert Moshe Fishman on 5/30/2023.

There is no magic timing to switching auto insurers, but some people look for a new insurer when renewal time comes around. Other reasons can include price and customer satisfaction.

There may also be life changes that will affect your policy. Whatever the reason, today’s shoppers are also looking for convenience and value to get a better deal. And why not? You shop around for other things in life, why not insurance?

As far as timing, you can always switch your auto insurance carrier, even after being involved in an accident. However, you will still have to follow through on any outstanding claims with your previous insurance company.

If you do decide to change insurers, you will not be able to file a claim for your accident under your new policy. So, although you can shop around and switch for a new auto insurer at any time, it’s not always an ideal situation to do so at the time of the accident.

You may have other reasons that prompt you to want to make the switch, like the cost. But price isn’t the only reason people switch. A bad customer experience can also play a huge role in wanting to move to a new insurance company.

However, whatever your reasons, waiting until your policy renews may not always be the best option. According to Kelly Blue Book, you may be better off making your move sooner, prior to renewal time.

What this article covers:

What you should know:

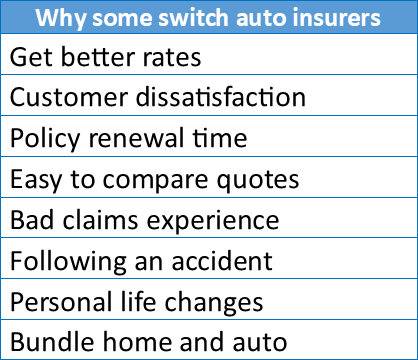

When it comes to auto insurance, rising rates and experiencing bad service are just two of the reasons people want to make a switch. But each person’s situation is different and their reasons to change will vary. Here are a few of the most common:

If you are moving to a new state, be prepared for a difference in premiums since there are huge variances among states. These differences are due to state laws, claim rates, number of uninsured motorists, and natural disaster frequency. According to Statista, “Michigan had the most expensive car insurance premiums at 5,740 U.S. dollars for minimum coverage as of June 2021.”

And the J.D. Power 2021 U.S. Auto Insurance Study, shows that customer service satisfaction is flat following four years of improvement. So, like many industries, people look for and expect good customer service.

Switching insurers is not a new phenomenon. Add the convenience of comparing insurance carriers and shopping online, and it’s not surprising that the trend to shop around has seen an increase.

There are many reasons why drivers decide to look at other insurance offerings. Life changes, for example, can happen at any time which warrants looking for a new policy and rate that’s best for you. The reality is that many variables can affect your premium and any potential savings. Here are some of the possible benefits:

Better rates – Auto insurers set their own pricing based on certain variables. These factors (changing variables) are the reason many experts recommend that you compare prices every six months before your policy term ends. Doing so could possibly get you reduced rates (up to 20% in some cases) and better meet your needs.

Better coverage – But equally important is getting the right coverage for your situation. You may find better coverages and discounts are available with a new insurer. The whole concept behind insurance is having protection when you need it most. Getting it right means choosing the company you feel has your specific needs in mind.

Better customer experience – If your current insurer doesn’t satisfy your standard of customer service, it may be time to compare companies. You deserve a better customer experience for the premiums you pay.

Discounts – When comparing rates of different auto insurance carriers, you should also inquire about any available discounts that might be available to you.

Before switching carriers, there are some things you should consider. For example, you’ll want to take into account any savings that you currently receive by bundling your home and auto coverage. Moving only your auto policy would eliminate that discount.

You’ll also want to take into consideration other savings that you might be receiving with your current insurer, like loyalty discounts (2%-5%), accident forgiveness, or vanishing deductibles. In addition, not all discounts that you currently receive may be available with the new insurer.

If your goal is to switch companies because of raised premiums as a result of an accident, you might be surprised. Your current car insurance company may actually be your best bet. This is due to the fact that companies have their own process of weighing your risk factors.

Wait until renewal time following an accident. Most states don’t allow changing premiums midway through your policy even though your insurer is aware of your accident. Your rates are likely to go up when your policy term ends, which is a good time to shop around. You may find a company that doesn’t consider your accident as severely when figuring your rates.

With your written notice, most insurance companies will give you the right to cancel at any time during your policy term. However, some insurers do charge a cancellation fee for doing so before your policy ends. This penalty may be a flat fee or as much as 10% of any remaining policy premiums.

You should receive a pro-rated refund for any remaining prepaid premiums that were unused if you cancel your policy midterm. You’ll want to factor in the cancellation fee to see if canceling before your policy ends makes financial sense.

It’s a good idea to get a written confirmation of your cancellation so your policy won’t renew automatically and billing will stop.

Also, be sure you have a new auto policy in effect before canceling your old one. This is to ensure you are covered without any lapses in insurance. A lapse of coverage can make you a higher risk, raise your rates, and is against the law in some states, where you can't drive without insurance.

Changing to a new carrier is not difficult. In addition, doing so does not hurt your insurability if you do it right. Here are a few easy steps to follow:

Finding the right insurance company shouldn’t be difficult. If you are looking to change your auto insurer, start your search today.